In a world where digital currencies are becoming mainstream, RedotPay stands at the forefront, transforming how we handle our crypto assets. RedotPay bridges the gap between cryptocurrencies and everyday spending, making it as easy to use your digital assets as traditional fiat money.

Seamless Integration

RedotPay offers both virtual and physical cards that are widely accepted across 44 million merchants globally. Whether you’re paying for a coffee, booking a flight, or shopping online, RedotPay ensures your crypto transactions are smooth and hassle-free. With compatibility with Apple Pay and Google Pay, you can use your digital wallet on your smartphone without needing to convert your crypto into fiat currency in advance.

Instant Transactions

One of the standout features of RedotPay is its instant transaction capability. Unlike traditional banking systems that can take days to process transfers, RedotPay enables real-time payments. This feature is particularly beneficial for those who need to make quick transactions without the wait time typically associated with crypto conversions.

Security You Can Trust

Security is paramount when it comes to managing digital assets. RedotPay provides robust custodial services with $50 million insurance coverage, giving you peace of mind that your assets are protected. The platform’s advanced security measures ensure that your transactions and personal data remain safe.

Zero Fees

RedotPay offers fee-free crypto transfers, making it an economical choice for users. You can transfer your digital assets without worrying about hidden charges or additional costs. This feature is particularly advantageous for regular users who want to maximize the value of their assets.

User-Friendly Experience

Designed with the user in mind, RedotPay’s platform is intuitive and easy to navigate. Whether you are a seasoned crypto enthusiast or a newcomer to the digital currency world, RedotPay makes the process straightforward and user-friendly.

Expanding Horizons

As cryptocurrency adoption continues to grow, RedotPay is committed to expanding its services and staying ahead of the curve. By continuously innovating and adapting to market needs, RedotPay ensures that it remains a leader in the crypto payment space.

Conclusion

RedotPay is more than just a payment platform; it’s a gateway to the future of financial transactions. With its wide acceptance, instant transactions, robust security, and zero fees, RedotPay offers a comprehensive solution for all your crypto payment needs. Embrace the future of payments with RedotPay and experience the convenience and security of using your crypto assets anytime, anywhere.

Currently, Redotpay does not provide support to residents of certain countries and regions, including Afghanistan, Belarus, Burma (Myanmar), Burundi, Canada, Central African Republic, Mainland China, Cuba, Darfur, Democratic Republic of the Congo, Eritrea, Ethiopia, Guinea-Bissau, Haiti, Iran, Iraq, ISIL (Da’esh), AI – Qaida and the Taliban, Lebanon, Liberia, Libya, Mali, Nicaragua, North Korea, Russia, Rwanda, Sierra Leone, Somalia, South Sudan, Sudan, Syria, Ukraine, United States, Venezuela, Yemen, Zimbabwe residents.

Disclaimer: Always conduct your own research before investing in or using any financial services. The information provided here is based on the features available at the time of writing and may be subject to change.

Web3 and metaverse have been two buzzwords for the year 2022, but according to the World Economic Forum, Web 3 is essentially a synonym for the metaverse. Therefore, I wish to discuss the two concepts together instead of writing two articles.

What is Web3.0? It can simply be understood from the following aspects:

Web1.0 is “read-only”;

Web2.0 is “readable + writable” (read + write);

Web3 is “read+write+own” (read+write+own).

Firstly, web1.0 is represented by websites Yahoo and Sina, which solely provide information to users . During this era, most users can only read information on the web while very few website developers could create content, I was one of them. I created my first website in 1995 titled ‘Visual Basic Tutorial” which still ranks top in Google search for the keyword ‘Visual Basic’. Web2.0 is an interactive web comprising blogs, social media like Facebook, Instagram, Twitter, Whatsapp, WeChat, Tiktok and more, which users can interact and generate content. On the other hand, web3.0 not only allows users to generate content but the content data is owned by the user, not controlled by the platform.

Secondly, we can define the web revolution by the degree of decentralization. Simply put, web1.0 is semi-centralized, Web2.0 is centralized and web3 is fully decentralized.

Comparison between Web 1.0, Web 2.0 and Web 3.0

In the Web1.0 era, decentralized personal websites formed half of the Web while the other half were centralized, both sides formed a semi-decentralized ecosystem. In the Web2.0 era, information islands are formed, and large companies such as FAANG monopolize the web and control users’ data and while numerous individual and SME websites formed a small portion of the web. On the other hand, web3.0 will be purely decentralized where data is owned and controlled by users. Web 3 is a concept for the next generation of the internet. It is the evolution of how users are able to control and own their creations and online content, digital assets and online identities. In Web 3, however, users can create content while owning, controlling and monetizing them through the implementation of blockchain and cryptocurrencies.

Data privacy is another issue of the current Web 2.0 internet. While the centralized entities have full control over the access to the service, they have full control over the users’ data. Users register to access a service and give up their precious private data and content in exchange for the convenience of the service, by agreeing to the terms of services. However, in Web3, not a single entity has control over the access to the service as it’s open to everyone. No registration is needed, users then have complete control over their private data, but at the same time, users have to take the responsibility to protect their own data and assets as they will become the only custodians.

The third aspect:

Web1.0 and Web2.0 are information Internet while Web3 is the Internet of Value. Web1.0 and Web2.0 are essentially transmitting information and focusing on consumption; while Web3 is transmitting value and creating wealth. Therefore, Web3 can be simply understood as the Internet powered by blockchain technology. It will solve the current Internet “central monopoly” problem, help users regain their data sovereignty, and recreate a better ecosystem in the digital world. Internet world. If you really understand the above changes, then you will understand that Web3 is revolutionary.

Key features of Web3 are:

Decentralized

Web3 data are typically stored in decentralized ledger like blockchain, so no single system has access to it all. It is dispersed across multiple platforms. This facilitates decentralized access and eliminate single point of failure .

Permissionless

The decentralized web can be accessed by users without requiring special permissions and KYC. Users will not need to disclose their personal information to access specific services. There will be no need to compromise privacy or share any other information.

Secure

Web 3 is more secure since decentralization makes it more difficult for hackers to target specific databases. Besides that, all data are encrypted based on cryptographic hash which add a security layer to the distributed database system.

Why we don’t call web3 as web3.0? Because they are fundamentally different.

Differences between web3 and web3.0

Web 3.0 aka semantic web focuses on efficiency and intelligence by reusing and linking data across websites. Web3 aka the decentralized web, however, puts a strong emphasis on security and empowerment by returning control of data and identity to users.

Semantic web uses a central place called the solid pod to store all user data, enabling users to handle third-party access to their data. Solid pods also issue a unique WebID for users that act as an identity within the ecosystem. In the blockchain-based web3, users can store their data in a cryptocurrency wallet, which they can access using their private keys.

Additionally, they both use different technologies to implement their purpose of data security. Web3 uses blockchain technology, while in web 3.0, certain data interchange technologies like RDF, SPARQL, OWL, and SKOS are used.

Data in web3 is difficult to modify or delete since it is scattered across multiple nodes; however, data in web3.0 can be changed effortlessly. Furthermore, the data stored in the solid pod is centralized, while the keys stored in crypto wallets provide access to the data of assets that reside on a blockchain

The differences are summarised in the following table:

Parameter

Web3

Web3.0

Distribution Model

Decentralized peer-to-peer

Client/Server

Protocol

Blockchain/ipfs

http/https

Relationship to World Wide Web

An Alternative to the World Wide Web

The continuation of the World Wide Web

Vision

Eliminates intermediaries and emphasis on security and empowerment by returning control of data and identity to users.

Evolving to a semantic web to make web content machine readable.

To learn more about Web3, please check out my book:

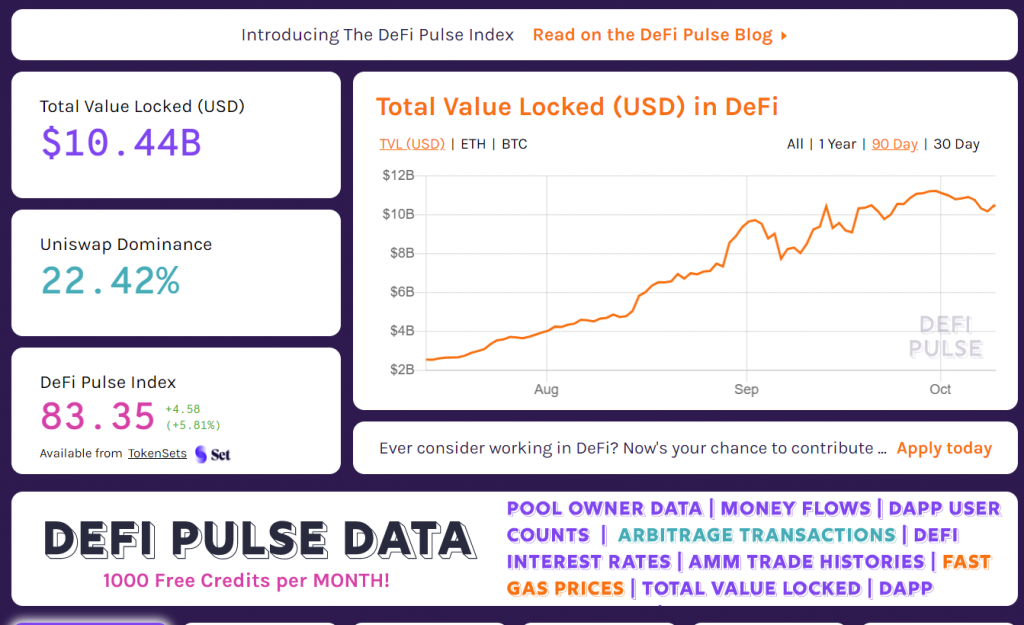

DeFi and Yield Farming have been the most popular buzzwords among the crypto community in recent months. Some DeFi tokens can skyrocket to more than 10K USD in just a few days but drop back to near zero also in a matter of days! Besides that, people in the crypto community are talking about yield farming instead of mining nowadays, most of you might scratch your head and wonder what the heck is that? Skeptics might challenge that DeFi is merely hype, but the total value of digital assets locked in the DeFi platforms has reached an astounding $10 billion(as seen in the figure below), thus it has created huge DeFi economics(Should I call it DeFiconomics?).

Source: https://defipulse.com/

To help you understand DeFi and Yield Farming, I shall try my best to explain these two concepts in a nutshell.

What is DeFi?

The word DeFi stands for decentralized finance, which means operating financial applications on a decentralized platform such as blockchain. It is the new financial architecture that leverages decentralized networks and decentralized technologies such as smart contracts to transform old financial products into trustless and transparent protocols that run without intermediaries. DeFi has a popular nickname ‘Money Lego’ because of the process of DeFi development like building legos where different components of a system can easily connect and interoperate.

DEFI Features

DeFi has unique features compared to CenFi (Centralised finance) and claimed to be able to provide more convenient and seamless services, particularly for the underserved people. Here are some of the features:

P2P- Transactions are performed on peer to peer basis without the need for intermediaries

No need KYC- Anyone can open an account with a DeFi platform anytime and easily without going through the tedious and painful process of KYC

No one holds your digital assets- DeFi platforms are non-custodian in nature which means they do not hold your private keys, you have full control of your own digital assets.

DeFi Products

Popular DeFi products include decentralized exchanges, loan and savings markets, tokenized physical assets such as gold, derivatives, forecasting/betting markets, payment networks, insurance and more.

Loan and Savings Markets

DeFi loan and savings markets allow you to lend, borrow, or deposit money in a platform. Among the popular loan and savings platforms are Compound, Aave, MakerDAO, Dharma, dYdX, and more.

Compound

Compound is a protocol on the Ethereum blockchain that creates a money market, which is a group of assets with algorithmically earned interest rates, based on supply and demand for those assets. The asset provider (and borrower) interacts directly with the protocol, earning (and paying) floating interest rates, without having to negotiate conditions such as maturity, interest rates, or collateral with peers or business partners.

MakerDAO

MakerDAO is a smart contract that allows users to open Protected Debt Positions, or CDP (Collateralized Debt Positions). Users deposit ETH as collateral and can mint or borrow tokens called DAI. DAI is a stablecoin linked to the US dollar.

Borrowers pay an annual interest rate called the stability fee to mint a new DAI. After the debt is repaid, the DAI is burned along with the stability fee owed in the MKR Maker token. Stability charges prevent users from overspending the amount of DAI supply in excess.

Aave

Aave is a decentralized non-custodial money market protocol in which users can participate as depositors(lenders) or borrowers. Depositors provide liquidity to the market to earn passive income, while borrowers can borrow in an overcollateralized or undercollateralized manner.

Dharma

Dharma is an open-source lending and savings account built on Compound which is characterized by its ease of use and simplicity. Dharma features a Smart Wallet is a non-custodial that automatically lends out any DAI or USDC it receives on Compound and generates a variable interest rate. Dharma requires users to have a fully verified Coinbase Account in order to create a new account.

dYdX

dYdX is a non-custodial trading platform on Ethereum that caters to more experienced traders. The dYdX platform allows users to lend, borrow, or margin trade any supported asset like ETH, Dai, USDC, and more. Interest rates vary by asset and adjust with supply and demand. Interest continuously accrues and is paid to lenders, minus 5% which is set aside for dYdX’s insurance fund.

All borrowed funds must initially be collateralized with 125% of their value. Liquidation occurs if that ratio falls below 115% and comes with a 5% penalty. Traders can take leveraged long positions of up to 5x their collateral’s value and 4x for shorts. Loans and margin trades can remain open for a max of 28 days, after which they are automatically closed out with a 1% expiration fee.

Decentralized Exchange

Decentralized exchanges or DEX are like stock exchanges but run by smart contracts on the Ethereum blockchain. While both allow you to trade assets, decentralized exchanges only trade cryptocurrencies and do not require centralized authorities to operate. Some of the popular exchanges are Uniswap, SushiSwap, Bancor, Kyber, Balancer, and more.

Uniswap

Uniswap is a decentralized ERC-20 token exchange that supports Ethereum and ERC20 tokens. The advantage of Uniswap is that you can exchange ETH with other ERC-20 tokens in a decentralized way. No companies involved, no KYC, and no intermediaries.

The Uniswap platform is unique in that it does not use an order book to derive the price of an asset or to match buyers and sellers of tokens. Instead, Uniswap uses the Liquidity Pool which comprises a group of tokens managed by smart contracts. The liquidity pool ensures enough tokens for users to exchange with each other using Ethereum as a channel.

Bancor

Bancor is a protocol on Ethereum for non-custodial token exchange using pooled liquidity. Bancor does not use order books, Instead, it uses an algorithmic market-making mechanism through the use of Smart Tokens. This will ensure liquidity and accurate prices by maintaining a fixed ratio among connected tokens and adjusting their own supply.

The Bancor platform has expanded beyond Ethereum to offer an exchange with EOS and POA Network. It also features a native token known as BNT( Bancor Network Token), which serves as a Smart Token hub that connects all other tokens in the Bancor Network, enabling instant trades among any asset supported by Bancor.

Kyber

Kyber Network is an on-chain liquidity protocol that allows the token holders to contribute liquidity known as reserves. The Kyber Network offers multiple types of reserves that exist in smart contracts. Besides that, Kyber does not use order books; when a user initiates a trade, Kyber returns the best price across all reserves.

The Kyber Network can be integrated into dApps to enhance user experience. In addition, Vendors and wallets can also use the Kyber Network to allow users to transact using their token of choice in a single transaction. Moreover, Kyber has a native token called KNC which is used to align ecosystem incentives. Holders can stake KNC to participate in governance and earn rewards, reserve managers pay fees and receive rebates in KNC, and DApp integrators receive a portion of fees.

Balancer

Balancer is an automated market-maker built on Ethereum. It allows anyone to create or add liquidity to customizable pools and earn trading fees. Instead of the traditional AMM model, Balancer’s formula allows any number of tokens in any weights or trading fees.

In fact, Balancer is like an inverse of ETF: instead of paying fees to portfolio managers to rebalance your portfolio, you collect fees from traders, who continuously rebalance your portfolio by following arbitrage opportunities. Balancer protocol is designed to be composable and has three types of pools:

1) Private Pools where only the owner can contribute liquidity and has full permissions over the pool, being able to update any of its parameters.

2) Shared Pools where the pool’s tokens, weights, and fees are permanently set and the pool creator has no special privileges. Anyone may add liquidity to shared pools and ownership of the pool’s liquidity is tracked with a specific token called BPT – Balancer Pool Token.

3) Smart Pools which are a variation of a private pool where the controller is a smart contract, allowing for any arbitrary logic/restrictions on how pool parameters can be changed. Smart pools may also accept liquidity from anyone and issue BPTs to track ownership.

Yield Farming

Yield farming is an activity that uses crypto assets to generate as much return as possible on those assets. A yield farmer may continually chase which pool offers the best APY (Annual Percentage Yield). This may mean moving to risky pools from time to time, but yield farmers can deal with the risks.

In some sense, yield farming is similar to staking but is a lot more complex. In many cases, it works with users called liquidity providers (LP) that add funds to liquidity pools. For example, a yielding farmer puts 100,000 USDT into the Compound. In return, he or she will get a token for the stock, called cUSDT.

Let’s say he or she get 100,000 cUSDT back. He or she can then put the cUSDT into a liquidity pool that uses cUSDT in Balancer, an AMM (auto market maker) that allows users to set up a crypto index fund that is rebalancing. At normal times, this can earn a small amount of transaction fees. This is the basic idea of yield farming. Users are looking for sophisticated cases in the system to produce as many results as possible in as many products as possible.

Liquidity Pool

What is a liquidity pool? It’s basically a smart contract that contains funds. In return for providing liquidity to the pool, LPs get a reward. That reward may come from fees generated by the underlying DeFi platform, or some other source.

Some popular Yield Farming platforms are SushiSwap, Yearn Finance, and YAM Finance.

SushiSwap

SushiSwap is an automated market making (AMM) decentralized exchange (DEX) currently on the Ethereum blockchain. Unlike other protocols, SushiSwap is a community-run project that is governed by the vote of the community. There are a few core products for SushiSwap’s ecosystem:

Each of these serve a different purpose within the ecosystem. Users Earn SUSHI tokens by staking SushiSwap V2 SLP Tokens.

Yearn Finance

yearn.finance is a decentralized ecosystem of aggregators that utilize lending platforms such as Aave, Compound, Dydx, and Fulcrum to optimize your token lending. When you deposit your tokens into yearn.finance, they are converted to yTokens. yTokens are periodically rebalanced to choose the most profitable lending services.

Among the aggregators, Curve.fi is the most prominent integrator of yTokens. Curve.fi creates an AMM between yDAI, yUSDC, yUSDT, yTUSD that not only earns the lending fees but also the trading fees on Curve.fi. On the other hand, YFI, yearn.finance’s governance token, is distributed only to users who provide liquidity with certain yTokens. With no pre-mine, pre-sale, or allocation to the team, YFI is claimed to be the most decentralized token in the DeFi space.

YAM Finance

YAM Protocol is a decentralized cryptocurrency that uses a rebasing mechanism to raise funds for a treasury managed by the community. The community can then use those funds via YAM governance to build the protocol.

In addition, YAM is the governance token for the YAM protocol. Using token voting, YAM holders have direct influence over the YAM treasury and direction of the protocol. Governance discussions take place on the Yam Governance Forum.

Currently, you’re able to earn YAM rewards by providing liquidity to the yUSD/YAM Uniswap pool. The rewards given to the pool are 92,500 in week 1, decreasing by 10% every week after. Please realize that you must apply the YAM scaling factor to get the current reward amount at any given time.

Conclusion

In short, DeFi is the most exciting blockchain-based financial ecosystem right now, but it is also extremely risky and confusing. This article is just an introduction to DeFi and I hope you could understand the basic concepts. To help everyone understand the DeFi applications better and even use them to accumulate wealth in digital assets, I will attempt to write a series of article of DeFi that shall zoom into some famous DeFi platforms like Compound, UniSwap, SushiSwap, yearn finance, Balancer and more, stay tune!

Cross-border money transfer is a huge market. According to World Bank statistics, the scale of global cross-border payments has grown at an average annual rate of 5%. Global remittances grew to $689 billion in 2018 and $717 billion in 2019 and projected to reach $750 billion in 2020.

Remittances represent a steady supply of foreign funds for many low- and middle-income countries and play a vital role in lowering the level of poverty (Digital Financial Services, 2018). Remittances support demand for local consumption and complement the volatile flows of other types of international funds, such as foreign direct investment and aid. At the household level, remittances are associated with increased spending on housing, education, and income-generating activities. Thus, remittances play an important role in the economic growth of low- and middle-income countries.

However, due to the large number of intermediaries involved, the cost of cross-border remittances is prohibitively high, the average commission rate per remitter is as high as 7.68%. In addition, the remittance cycle is long, from a few days to weeks or even months. Moreover, existing cross-border remittances also suffer from other issues such as frauds, exchange rate losses, counterparty risk, red tape and more. On top of that, an estimated 2 billion people are unbanked and therefore being excluded from the existing global financial services, including cross-border money transfer. As a result, a large proportion of remittances are still sent through informal channels, which lack consumer protection mechanisms (Digital Financial Services, 2018). In short, transferring money across international borders is still complicated, time consuming and expensive.

Fortunately, the proliferation of innovative digital technologies is rapidly transforming the remittance landscape. Innovative technology-based remittance models are slowly replacing incumbent, clunky and costly models. On the one hand, these new models help to reduce transfer costs and time and improve access at both the sending and receiving ends. Let us examine several emerging business models for cross-border money transfer.

Emerging Models for Cross-Border Remittance

Remittance Model

Description

Mobile Money

Cross-border remittances are sent through mobile money or e-wallet accounts. The transfer can happen between: – Providers owned by the same group holding company.- Different providers working in cooperation. -Multiple providers connected through a “hub” operated by a third party. -Mobile money/e-wallet accounts can be used by the senders and the receivers.

Online

Users transfer money through an online remittance platform. The transfer can be made through the provider’s mobile phone app or website. Senders can use their online banking account, debit card, credit card and more to link to the platform to send money. Receivers can receive funds in several ways, such as mobile money, bank account deposit, airtime top-up or cash pick-up.

Peer-to-Peer

This is a fully online model as no cash is accepted or sent out. Transactions can happen only through a bank account, card or closed loop wallet offered by the provider. As the cross-border movement of money is low, the cost of remittances is also relatively low.

Blockchain

This blockchain-based model enables money transfer in the form of cryptocurrencies like bitcoin, Ethereum and more. Funds are sent and received in the respective local fiat currency, but the cross-border transfer of funds happens through blockchain in the form of digital cryptocurrency. For examples, platforms such as Ripple and Ethereum enable cross-border payment services through their own cryptocurrencies (XRP and Ether, respectively) or through their platforms based on blockchain technology. Blockchain provides a decentralized ledger of transactions (blocks) distributed among all members of the network (chain). The ledger is updated every time a transaction takes place once verified and approved by the nodes in the blockchain network.

Among the emerging remittance models, blockchain-based remittance is the most promising and has the greatest potential to disrupt the conventional cross-border money transfer business.

The blockchain-based remittance model has the potential to enable the unbanked people and migrant workers to send money fast and at low cost back home.

Blockchain technology can solve the pain points of high cost and delay of cross-border remittance. Indeed, blockchain-based remittance can simplify the entire process, removing unnecessary intermediaries and other barriers. The idea is to provide frictionless and near instant payment solutions. Unlike traditional services, a blockchain network need not rely on a slow and tedious process of approving transactions, which usually goes through several banks and intermediaries.

A blockchain remittance system can perform worldwide financial transactions based on a distributed network of computing devices known as nodes. This means that several nodes participate in the process of verifying and validating transactions which can be done in a decentralized and secure way. The encryption feature of blockchain provides security and an easily verifiable public audit trail. Better security means less frauds that are rampant in traditional banking. Overall, blockchain technology can provide faster and more reliable payment solutions at a much lower cost.

Let us examine some blockchain architectures and use cases pertaining to cross-border money transfer.

Stellar

Stellar is an open-source network for currencies and payments. Stellar makes it possible to create, send, and trade digital representations of all forms of money—USD, SGD, Euro, Bitcoin, ETH, and more. It is designed so all the world’s financial systems can interoperate on a single network. Stellar is a borderless, limitless, and powerful open network for storing and moving money

Stellar has no owner; it is owned by the public. The software runs across a decentralized, open network and handles millions of transactions each day. Like Bitcoin and Ethereum, Stellar relies on blockchain to keep the network in sync, but the end-user experience is more like cash—Stellar is much faster, cheaper, and more energy-efficient than typical blockchain-based systems.

Stellar makes it possible to create, send, and trade digital representations of all forms of money: dollars, pesos, bitcoin, pretty much anything. It’s designed so all the world’s financial systems can work together on a single network.

Though Stellar is cryptocurrency-centric, it has always been intended to enhance rather than replace the existing financial system. In contrast to the Bitcoin network that was made for trading only bitcoins, Stellar is a decentralized system that was designed for trading any kind of money in a transparent and efficient way.

Stellar has a native digital currency, the lumen, that is required in small amounts for initializing accounts and making transactions. However, other than those requirements, Stellar does not privilege any specific currency. It is specifically designed to make traditional forms of money more useful and accessible.

With Stellar, you can create a digital representation of a fiat currency of any country. Essentially, you can set up a 1:1 relationship between your digital token and fiat currency. Every one of your tokens out in the world is backed by an equivalent fiat deposit. So while people hold the tokens, they can treat them just like traditional money, because they know that they’re exchangeable for traditional money in the end.

Everex

Everex is a global blockchain fintech company headquartered in Singapore with offices in Bangkok/Thailand. It facilitates the application of Stablecoins for peer-to-peer money transfers, merchant payment settlements and fiat to digital asset exchange. Exverax focuses on fiat and asset pegged Stablecoins that represent units of national currencies and international investment assets that are powered by smart contracts and exist in Ethereum blockchain token format.

Everex is operating on Euro, British pound, Thai baht and Stablecoin markets with the main office in Bangkok, Thailand. Its solution allows 25x faster seamless transaction settlements for global and domestic payments with virtually zero cost, providing users with more efficient access to funding. Everex implements Ethereum blockchain technology as a new rails for financial transactions to challenge existing legacy payment system solutions and also to address the growing global financial inclusion problem.

Everex enables transparent cross-border financial transactions, bringing individuals and SMEs – with or without bank accounts – into the new global economy powered by the distributed ledger technology. The blockchain technology eliminates the need of any third-party or central authority for financial transactions, by encrypting and storing transactions in participants’ account ledger, making it almost impossible to tamper.

The main product is a blockchain-based mobile wallet which enables end users to instantly convert and send money abroad – for which the company offers a white-label solution to any interested parties like banks, central banks, and many others, which offer cross-border money transfers.

Furthermore, Everex deploys blockchain technology using smart contracts to digitise national fiat currencies in order to enable instant money transfer over the blockchain. It has created a price-stable coin called eFiat which is a full representation of a national currency on the blockchain, fully-pegged by its fiat value (meaning that 1 EUR = 1 eEUR). This solution enables cryptocurrency exchanges to better deal with their liquidity and cash-in/cash-out options.

MoneyFi

MoneyFi addresses the growing and emerging market demands for a better alternative in remittance based on the deployment of the secure credit cards. Its non-traditional approach, using blockchain technology, is purpose-built to drastically reduce transaction fee costs, providing financial inclusion for underbanked and unbanked people, leveraging the worldwide ATM’s platform’s rapid expansion rate of its network.

MoneyFi intends to disrupt this market with blockchain. The MoneyFi platform is a communication channel for cross border currency remittances based on digital assets trading. Users will be able to remit money via the MoneyFi App that uses its native cryptocurrency token “Nemoo” for settlement. The App is integrated into an existing infrastructure consisting of a global ATM processing network that will facilitate newly developed fiat-crypto hybrid ATMs.

Cryptocurrency is a new asset class derived from nascent blockchain technology. Its phenomenal growth in recent years has attracted many investors who used to invest in traditional financial products to start investing in crypto assets. Reports have shown that there is a significant amount of capital flowing into the crypto market. This capital flow has created an increasing demand for new financial products that cater to the needs of the crypto market.

Indeed, cryptocurrencies are rapidly gaining traction with the general public. According to CoinMarketCap, the total market cap for all cryptocurrencies reached an amazing $739 billion in January 2018. Though the market cap dropped to a low $113 billion in December 2018 due to the bear market, it rebounded strongly in 2019 to a figure between $250 billion to $350 billion. Though much of this value has been generated by individual traders, it is also largely the result of large investment funds. These crypto fund management companies, which hold crypto assets worth as much as $1 billion or more, are the whales of the cryptocurrency community.

Generally, the trading of crypto assets is performed on exchanges. Most crypto investors keep and manage their crypto assets on exchanges, cold storage, mobile wallets, desktop wallets, hardware wallets, and more. The aforementioned complex management process that requires sophisticated skills makes it extremely difficult for individuals to manage a diverse crypto portfolio.

Fortunately, a dozen crypto fund management companies have emerged with products and services that could help ease the tedious investment process in crypto investment. One of the most popular ones is the use of index funds to automate the process of investing in crypto assets for individuals, using AI algorithms. Another crypto financial product on the rise is the crypto hedge fund which caters only to high net worth individuals.

Indeed, crypto investment tools and products such as crypto index funds, automated trading with rebalancing, and tracking are becoming ubiquitous. Crypto index funds provide an opportunity for investors to build their own portfolio or track an index and reap profits from this new and volatile asset class.

Despite the potential issues, it’s encouraging that crypto hedge funds seem to have performed reasonably well even during bear markets. And with the majority of crypto funds in the index now employing external auditors, custodian services and fund administrators, the industry is becoming less risky. Although the crypto fund industry is still very much in a nascent stage, crypto funds could present institutions and individuals with an attractive way to invest in this sector.

Let’s examine some index funds in the crypto market.

Bitwise 10 Private Index Fund

The Bitwise 10 Private Index Fund is the world’s first crypto asset index fund. It seeks to track the Bitwise 10 Large Cap Crypto Index (“Bitwise 10 Index”), which selects the 10 largest crypto assets based on criteria including 5-year diluted market capitalization, trade volume minimums, concentration limits, and compliance. The portfolio is rebalanced monthly. Assets are held in 100% cold storage, audited annually, and purchased across several liquidity providers to seek best execution. Bitwise actively evaluates network opportunities including hard forks, airdrops, emissions, staking rewards, super- and master-node rewards, and captures available benefits for fund investors where appropriate.

Bitwise is a crypto asset manager founded in 2017. The firm has a large software team, with backgrounds across Google, Facebook, Wealthfront, and military software security, which we believe is essential for navigating the space. Bitwise has been covered by CNBC, Forbes, Bloomberg, Barron’s, WSJ, Coindesk, and others, and is active in the crypto asset community

BITWISE 10 INDEX COMPONENTS

Bitcoin

BTC

77.8%

Ethereum

ETH

8.5%

Ripple

XRP

6.0%

Bitcoin Cash

BCH

2.4%

Stellar Lumens

XLM

0.6%

Litecoin

LTC

1.9%

EOS

EOS

1.4%

Monero

XMR

0.5%

Cardano

ADA

0.4%

DASH

DASH

0.4%

Crypto20

Crypto20 claims to be the first tokenized index crypto index fund in the world. Their motto is autonomous ‘token-as-a-fund’.

In 2017, their team successfully pioneered the first tokenized crypto-only index fund, which used the seed funding to buy the underlying crypto assets. There are no broker fees, no exit fees, no minimum investment and full control over your assets.

Crypto20 provides a way to track the performance of the crypto markets as a whole by holding a single crypto asset. They claimed that their index funds have consistently beaten the average managed fund since their inception.

Alternatively, you can look into more accessible funds that don’t require heavy investment. Let’s take a look at the following funds:

Coinbase

The Coinbase Bundle offers a one-click purchase for the first five cryptocurrencies that were listed on Coinbase, which are weighted by market cap at the time of purchase.

Bitcoin — 76.59%

Ethereum — 15.84%

Litecoin — 3.94%

Bitcoin Cash — 3.11%

Ethereum Classic — 0.52%

This retail-aimed product allows users to invest as little as $25 in the basket of crypto assets.

Hodlbot

HodlBot is a customizable cryptocurrency trading bot that enables users to index the market, create custom portfolios, and automatically rebalance their cryptocurrency portfolios.

HodlBot allows you to grow your portfolio like the world’s most sophisticated investors. They are making institutional portfolio management software available to everyone. Best of all, HodlBot is free forever for account values under $500. Otherwise, it’s $10/month with a 7-day free trial.

In short, crypto index funds are a fast-growing alternative financial product that is currently outperforming the stock markets and other traditional financial products. Though it is still riskier than traditional investments, it is worth venturing into this market to grow your capital.